MSTR, mNAV, and the Future of Bitcoin Treasuries

A Philosophical Dive into the True Value of Bitcoin Treasury Companies

Hey everyone, and welcome back to the On-Chain Mind Newsletter.

There are a few concepts in finance that most of us accept without ever really questioning them. Things like price-to-earnings (P/E) ratios, “fair value” metrics, or even the assumption that money itself holds steady value over time. But when you take a step back, some of these ideas start to look less like immutable laws of nature and more like collective beliefs propped up by tradition.

This article takes a deep dive into Strategy (MSTR), the idea of market-to-Net-Asset-Value (mNAV), and how these concepts fit into the evolving world of Bitcoin-focused corporations. It’s a more fundamental and philosophical look at this new type of company, drawing parallels with familiar ideas from traditional finance (TradFi) while questioning the assumptions many investors take for granted.

By the end, you’ll see why firms like MSTR aren’t just “buying Bitcoin” — they’re reshaping what shareholder value might look like in the decade ahead.

Let’s get into it.

Insights at a Glance:

Challenging Traditional Metrics: Free Cashflow per Share is the north star of traditional equity investing, and it has close parallels to Bitcoin per Share in treasury companies.

The Power of Growth Narratives: Investors bet on long-term growth despite unknowns, and this compliments Bitcoin’s superior compounding rates.

mNAV is the “new P/E”: It’s not just as a valuation tool, but as a signal of operational strength, funding prowess, and investor conviction in Bitcoin holdings.

Technical Signals for MSTR: Indicators like the 200D heatmap and Z-score Probability Waves highlight why MSTR’s current price near $350 offers a compelling entry point.

FCF/Share: The Traditional North Star

If you strip stock investing down to its essentials, one metric tends to rise above the rest: Free Cashflow per Share (FCF/share).

Why? Because free cashflow represents the actual cash a company generates after paying for operations and capital investments.

On a per-share basis, it is often considered the ultimate measure of a stock’s effectiveness at returning capital to its shareholders, whether through dividends, buybacks, or reinvestment. Sustained growth of 15% per year in FCF/share is often labelled “exceptional”, because compounding at that rate doubles shareholder value roughly every 5 years—a feat very few companies in the world consistently achieve.

This is why markets reward such companies with premium valuations, often in the range of 25–30 times earnings. In some cases, investors even stomach 100+ P/Es. That sounds absurd at face value—many won’t live long enough to see the implied payback period. But the rationale is simple: growth. If the story is compelling, investors will pay up.

The Madness of Growth Multiples

The willingness to pay huge multiples for earnings is one of the most widely accepted quirks in investing. Few stop to ask why. But if you step back, people are betting on an unknowable future.

Will the company even exist in 25 years?

Will it still dominate its industry?

Will earnings compounding persist uninterrupted?

Despite these uncertainties, the growth narrative itself becomes a kind of currency. Markets accept it as gospel.

The reason is because if many believe in the growth of a company, that narrative can drive a stock’s returns for years and years into the future. It’s a concept that is just widely accepted amongst the investing community, but when you break it down simply and just take a quick philosophical moment to think about what’s really going on, it’s really quite crazy.

The Rise of mNAV

Now, apply this logic to Bitcoin treasury companies. The same concept is playing out in the Bitcoin treasury company space at the moment. The mNAV (market-to-Net-Asset-Value) is the “premium” that investors are paying for a company to acquire more Bitcoin in an efficient manner that they themselves would not be able to achieve.

I like to think of it like the “new age” P/E (price-to-earnings) ratio. In fact, it is more conceptually similar to the P/B (price-to-book) ratio, though the term is less familiar to the average investor. Interestingly, the current P/B of the S&P 500 is about 5.4x, and its historical range has been between 1.5 to 5.5, eerily similar to MSTR’s historical mNAV.

P/B measures a company’s market price relative to its book value (assets minus liabilities). It tells you how much investors are paying for each dollar of net assets.

It’s honestly refreshing to see many investors questioning why we are paying a premium on the underlying Bitcoin holdings, rather than blindly accepting this concept like we do with many aspects of TradFi. We should be questioning why things are priced the way they are. And I think that is one of the overwhelming strengths of the average Bitcoin investor: the ability to question ideas that are widely accepted simply because “that’s the way things have always been done”.

So why do Bitcoin premiums exist at all?

Belief in the growth plan — the company will find ways to grow its stack faster than the individual could.

Access to cheap capital — which ordinary investors will never get.

Operational leverage — using structures like convertibles or equity raises to scale faster.

Can you get a loan at roughly 0% interest rate to accumulate more BTC? Almost certainly not. That is the power of the best Bitcoin treasury companies—and especially the larger committed players like Strategy (MSTR).

To contextualise, companies like MSTR leverage convertible debt, where lenders accept lower interest in exchange for equity conversion rights. This effectively subsidises Bitcoin accumulation. In TradFi, this mirrors how tech growth firms use leverage to scale without immediate dilution.

But if a FCF/Share growth of 15% per year in TradFi stocks is considered “exceptional”, why are we valuing a Bitcoin treasury company like MSTR at a 1.5x premium (or at worst a 4-5x premium) when Bitcoin has compounded at a compound annual growth rate of 60-80% over the past 5-10 years?

I think that is the main concept that has yet to be figured out by the wider investing community who are still largely unaware that Bitcoin is a Top 5 world asset and is slowly eating up the world’s capital value. And that’s a massive reason why I am bullish on the likes of MSTR over the long-term.

mNAV Discounts: Traps and True Signals

So can companies trade at a discount mNAV (i.e. below 1)? Well absolutely. According to Bitcoin Treasuries, of 167 publicly trading companies, 21 firms (roughly 13%) are trading at a discounted mNAV.

This again is very similar to why some stocks trade at crazy discounts, say a 5 P/E ratio. And many TradFi investors fall into this “value trap” where they believe they are getting a steal of a price because the stock is so cheap. But the real reason stocks are cheap, for most of the time, is because the company isn’t delivering the promises that investors are expecting.

The value trap concept I believe also applies to Bitcoin treasury companies. For those trading at a discount mNAV, it signals scepticism, perhaps related to:

Weak governance;

Fragile funding models;

Operational risks with their current business.

In fact, it also might point to the investor’s confidence in the companies’ ability to hold onto their Bitcoin holdings. Because, the mathematics shows that when an mNAV is below 1, it is actually accretive to the company shareholders to sell Bitcoin to buy back shares.

But firms like MSTR refuse that temptation. Even during the 2022 bear market, when their mNAV dipped below 1, they held their entire stack by restructuring debt. That’s why I am pretty certain that MSTR will not fall into this category. I have no doubt that they will keep hold of all their Bitcoin holdings, even when it is less optimal to do so. This HODL ethos stems from Michael Saylor’s vision of Bitcoin as pristine collateral.

I don’t share the same confidence with the other 166 publicly traded companies. The only other company I would throw into that HODL bucket is the Japanese firm Metaplanet.

So, mNAV isn’t a simple buy-or-sell trigger—it’s a perspective. A premium might signal conviction or just hype, while a discount could reflect trouble or hidden value. The key is context:

How effectively is the company increasing its Bitcoin per Share?

Has it got other revenue streams to back up the valuation?

How resilient is its funding model across market cycles?

MSTR’s Financial Wizardry

What really sets apart MSTR from the other plethora of Bitcoin companies is their diverse ability to raise fiat capital to purchase their BTC stack. Their low-cost funding tools like convertible notes and ever-expanding list of preferred share offerings can scale BTC holdings faster without diluting the average MSTR shareholder.

Convertible notes, for example, allow borrowing at near-zero effective rates if converted to equity during bull runs. This creates a flywheel: more BTC boosts collateral value, enabling more borrowing. Their financial wizardry warrants a decent premium, in my opinion. Just like NVIDIA warrants a decent P/E ratio in the TradFi world for their ability to scale their FCF/Share faster than almost any other company.

It’s just a completely brand new concept to most. Bitcoin treasuries are looking to expand their Bitcoin per share at the fastest rate, TradFi companies are looking to expand their free cash flow per share at the fastest rate. It’s the same idea. Except, one is looking to grow a form of pure capital that will appreciate at worst 30-50% per year for the foreseeable future, whilst the other is trying to accumulate their favourite fiat which erodes at 8-10% per year.

I know which one is likely to create more shareholder value given another 10 years of their strategies playing out.

Market Signals

Now to finish up, let’s quickly dive into some charts to uncover some potential value opportunities.

200-Day Heatmap Signals Strength: MSTR is poised to print its 2nd green dot this cycle on the 200-day heatmap, trading at its 200-day moving average of $353. This level, a critical support for bulls, marked the start of the bull run’s momentum. Holding here could signal a strong entry for upside potential.

Z-Score Probability Waves: MSTR’s price has dipped to the -2 standard deviation level, also at $353 weirdly. Historically, drops below -1 standard deviation have preceded explosive price action in this bull market, suggesting a high probability of mean reversion if macro bullishness persists.

Oversold Conditions: My Mean Reversion Oscillator, which has a similar logic to an RSI, shows MSTR in deeply oversold territory. Past instances at this level have often led to short-term bounces, if not significant rallies.

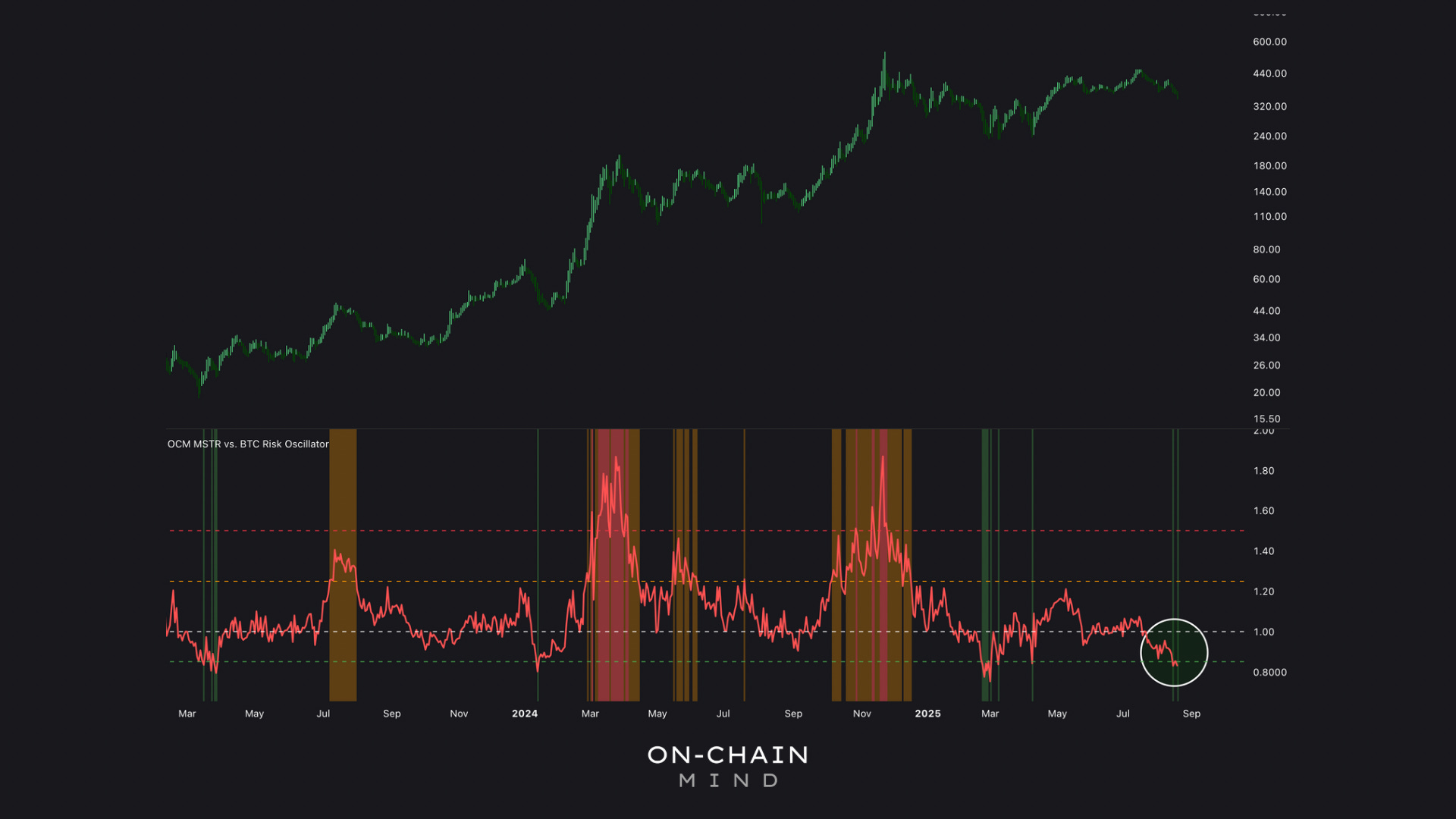

Bitcoin-Priced MSTR Opportunity: When priced in Bitcoin, MSTR’s risk oscillator is at one of its lowest readings, a strong signal for those in low-tax environments to rotate exposure from Bitcoin to MSTR. Historically, such lags in MSTR’s stock price relative to Bitcoin resolve with rapid catch-ups.

Why a Lagging MSTR Stock Price Doesn’t Worry Me

So to wrap all of this up, am I worried that MSTR’s stock price is lagging behind Bitcoin’s current price appreciation? Not in the slightest. The mNAV might be compressing to around 1.5 right now, but the real measure of its BTC game plan is still intact: their Bitcoin per share is still increasing every week. And for the most part, that is all I care about.

Just like traditional stocks, their free cash flow per share can be increasing year over year, yet their stock price can go up and down in fits and starts. That’s the beauty of irrational investor psychology. But if the fundamentals are increasing consistently over time (i.e. an increasing BTC per share), I will lavish at the opportunity to pick this company up at a discount. Because as we know, when investor sentiment flips, and the multiple eventually expands again, this stock has the ability to absolutely melt people’s faces off.

Key Takeaways

Question Valuation Norms: Just as TradFi accepts high P/E ratios for growth, Bitcoin treasuries deserve premiums for efficient BTC accumulation. Challenge why we scrutinise one but not the other.

Focus on Fundamentals: Bitcoin per share growth trumps short-term price lags; it’s the true north star, akin to free cash flow in fiat stocks.

MSTR’s Edge: Their funding innovation and HODL commitment set them apart, warranting optimism even in discounts.

Technical Opportunities: Current mean reversion indicators suggest MSTR is primed for a rebound, especially for Bitcoin-priced investors.

If you want to unlock the full picture — including access to my Custom Indicator Suite — consider upgrading to Premium 🚀

I’ll catch you in the next one.

Cheers,

OCM

🎥 Watch the video of this article on YouTube!👇🏼

Subscribe to the On-Chain Mind YouTube Channel!